OPM - Pension Edition

Other People's Money. OPM. Regular readers know by now that it's what politics is all about. How to get it, how to use it for personal gain, how to leverage it to achieve personal goals, and how to deny those one doesn't like access to it. Today's edition of the OPM files takes place in my neighborhood.

New York City's Comptroller, Brad Lander, has "urged" a number of consumer-goods giants, including Costco, Walmart, and Kroger, to become certified mifepristone dispensers. Mifepristone, aka RU-486, aka the “abortion pill,” is an oral medication that can terminate a pregnancy if taken in the first seventy days of gestation.

Lander warned these companies that they face "financial risk" if they don't.

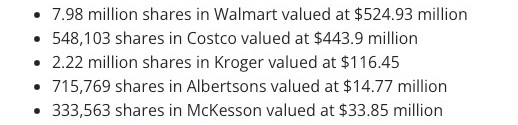

This isn't a friendly warning from a concerned citizen. In his role as Comptroller, Lander oversees NY City's pension fund, which manages $253B in assets on behalf of over 750K individuals who work or worked for the city. That total includes over $1.3B in total shares of the companies that Lander "urged." That the comptroller's web page devotes space to listing exactly how much of each of these companies is owned by the pension fund clarifies the sinister nature of this "urging."

Economist (and Great Man) Milton Friedman advanced a theory of business ethics that notes that the primary responsibility of a business's leadership is to the shareholders. This premise runs contrary to the "stakeholder" responsibility advanced by progressives in recent decades, and it is a premise I agree with. A shareholder has skin in the game. A shareholder voluntarily takes risk in investing in a company. A non-shareholding stakeholder, in progressive parlance, is someone who may be affected by a company's actions but does not bear financial risk.

Applied expansively, that would include all customers, all competitors' customers, and just about everyone else who might be worried about how a company's practices affect the environment, the labor market, or the economy overall. In normal business practice, all those subject to market forces and government regulation.

The "stakeholder" gambit is about imposing the preferences (moral and otherwise) of a preferred few on companies, rather than trusting the masses to decide for themselves what they want and how to "vote" with their own money.

This brings us to Lander's efforts. As Comptroller, Lander's sole duty with regard to the pension fund is to maximize its profits. That not only helps ensure pension promises are honored, it reduces the burden on taxpayers. Lesser profits may require tax dollars be injected into the system, meaning that taxes would have to be increased or that other tax-funded activities be curtailed.

Rather than honor that duty, Lander (and many other public pension managers) seek to go "beyond their brief," to use the power of billions of OPM dollars to bend companies to their will and to advance their agendas.

In this case, it's not even as if abortion access in New York City has been curtailed since the Dobbs ruling that overturned Roe v Wade. New York legislated the legality of abortion in 1970, three years before Roe. Since all Dobbs did was return the power of regulating abortion to the states, nothing has changed in New York. Lander's missive is about two things - keeping abortion a high-visibility issue ahead of the November elections, and (of course!) OPM.

I have refrained from discussing my personal views on abortion on this blog. I have explored the landscape, and have concluded that the matter boils down to the metaphysical question as to personhood. This makes it an issue that will never be resolved to satisfaction in American politics. Given that, and given the premise that government should be limited to a few well-defined roles, I argue that the government should not be in the business of funding abortion, nor should it be pressuring companies to "take sides" in the abortion debate.

This post isn't about abortion, however. Abortion is just one of many issues that pension managers have sought to exert influence. It's about the misuse of power to influence policy, and about the dereliction of fiduciary duty in favor of social engineering.

Individual shareholders have the ability to vote with their money, and since they incur personal risk in deploying their own money, it's OK to do so.

Public pensioners have no such ability, apart from their diffuse-to-the-point-of-nothingness ability to vote for NYC's Comptroller. Their money is captive, and they have no ability to redeploy that money if they are unhappy with its management.

Given that captivity, management should have an even greater sense of fiduciary duty than private company CEOs do. A private company's management might choose to take a risk by taking a social position in the hopes of leveraging current trends for fiscal gain. If some shareholders disagree, they can vote with their money. Public pension managers should be more circumspect, more respectful to the full spectrum of individuals whose money they are managing. Those individuals are hostages, unable to move their money elsewhere if they "don't like what you're doing with my money."

Whether it be about pressuring companies to sell abortion pills, about conforming to ESG folderol, or about demanding a company alter its business practices to satisfy political agendas, public pension managers improperly usurp the financial power of their captive "shareholders" when they stray from their strict fiduciary roles.

With(out) apologies to Glenn Frey,

It's the lure of Other People's Money, it's got a very strong appeal.

It's the ultimate enticement, it's the OPM blues...

Workers employed by a company and customers who depend upon a company's products don't have a financial stake in that company's success????