Unaffordable Housing

Have you heard about the housing crisis? Unless you're living under a rock, in which case you'd be an unlikely reader of this blog, you most certainly have. Young people today claim no hope of ever owning their own domicile, whether it be a house, a condominium, or a co-operative apartment, simply because housing has gotten too expensive. While a good bit of this may be perception - homeownership rates are about where they were 40 years ago - the factors that contribute to high home prices, and by extension, high rental costs, are real and worth discussing.

Many factors distortions, are "structural," in that they are imposed by government. While others, such as interest rates, are temporal (albeit often the result of government policy), it is the structural distortions that I want to look at today.

In that category, we find two sub-categories. While these may seem at odds with each other, they both drive prices the same direction: up.

First, there are the obvious cost-increasers. Building and zoning codes establish certain baseline requirements in the name of safety, sanitation, and access to public utilities, but those codes continue to grow year by year, and many new requirements aren't about safety as much as they are about other things. Those other things can include energy efficiency, even if the cost of that efficiency exceeds the benefit; building density; design mandates; climate change related mandates; and more. And that's just for new construction. Renovation of existing stock is also heavily influenced by zoning, and in many urban settings, by rent control regulations and by a stack of entities that have approval authority. I recently discussed how New York's laws keep tens of thousands of apartments off the market, simply because landlords are precluded from recouping the investment required to bring them up to rentable status.

Restricted supply and increased costs combine to make housing more expensive, but that's not the whole tale.

The other driver is the sheaf of distortions that benefit homeowners. These include the tax deductibility of mortgage interest and of property taxes, both of which can be considered, in a macro-taxation sense, a wealth transfer to homeowners. The same goes for flood insurance, which is underwritten by the federal government and which is actuarially way too low in many places. While the purpose of all this is to make ownership less expensive, market forces always adjust, and those distortions translate into higher home prices. It’s akin to government subsidizing college education: doesn’t make it cheaper, it just funnels more money to the universities.

Thus, we have an odd "push-pull" duo. Government pushes prices up via over-regulation, and government pulls prices up via favorable taxation and insurance underwriting.

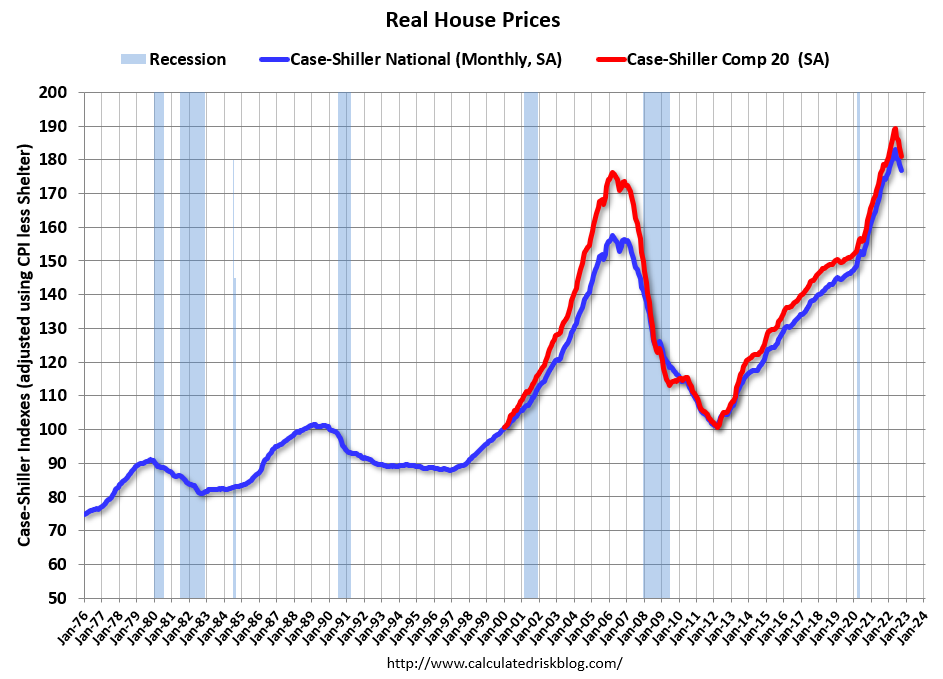

Consider this chart showing inflation-adjusted home prices across the past half century.

While new stock will be "better" in terms of energy efficiency and other ways, can we attribute a 130% increase simply to better quality? I don't think so.

What's to be done?

The "pull" side is a tough nut, since altering it too much could bankrupt enough homeowners to precipitate a crisis akin to 2008's. The much-maligned SALT cap, which is of greatest benefit to wealthy blue-staters, should stay, and flood insurance should slowly start to reflect financial reality. Killing the mortgage interest deduction is, on the other hand, both a political non-starter and a homelessness inducer, so I won’t bother suggesting it.

The "push" side might be a bit easier, though in many cases it'll face NIMBY opposition and much special interest squawking. Ease up on zoning restrictions that dampen new construction and renovation of old stock, ease up on building code requirements that aren't safety-related, and transition away from rent control schemes.

These remedies won't fix the problem in a week or a month or a year, but across a decade, they could make a real difference.

In 1986, I bought a house for 179000 after prices had doubled over three years during the “Massachusetts miracle. Interest rates were 12-14 percent. My payment was $2200 a month and my wife and I made a combined 55k a year. We didn’t take a vacation for 7 years or eat out much.

All just depends on your priorities.

There are, generally, great societal benefits to home ownership. It ties the new owners to a huge expense that forces them to work productively for an employer: lose your job, lose your house. Home ownership ties the owners to a community - it's not like renting where you can easily move and switch communities for something "better" - you'll want to improve your community since you cannot as easily move away. Homeowners will pour resources into "their" homes to keep them up - for resale value if nothing else. Home ownership accumulates wealth in the form of equity - it's a wealth acquiring plan - so in your Golden Years you've got, if nothing else, a big wad of cash that either transfers to your heirs (when they can really use it) or pays nursing home expenses.

Lots of benefits. So I get the government desire to incentivize ownership - we're all FOR more home ownership. But when the government incentivizes anything, it distorts markets. That's the downside. So, herewith, the conundrum. First, the government should "do no harm" - following the recipe you cited: stop with the idiot nonsense of regulating home ownership to the point of absurdity. If home ownership is seen as a community good - don't tax and regulate it to death. And insurance costs are now becoming prohibitive - which is driven by horrific inflation in construction materials. And interest rates - which are tied to federal government inflationary spending.

It seems just four short years ago, none of this was a problem.